When it comes to Strata Insurance, nothing is as simple as it seems. Lia de Sousa | Resolute Director, explains below the cover your clients need to adequately protect their properties and the contents inside.

If there’s one thing we’ve learnt from broking Strata Insurance for 40 years, it’s that there’s a lot of confusion about the various types of insurance cover required by people living in strata-titled properties. In short, it’s hard to know where one policy ends and the next begins.

There are 3 different types of insurance policies linked to strata living, but they all cover different aspects of your clients’ properties. Below, we help clarify the covers your clients need:

1. Strata Insurance

Strata Insurance – which is compulsory – provides general insurance cover for the building, shared or ‘common’ areas, common property and common contents – basically anything your clients and their neighbours own collectively, and which comes under the management of an Owners Corporation (OC) or Body Corporate.

Common property includes the building itself, and fixtures that form part of the building structure, such as fixed plant, machinery and underground services, and owners’ fixtures, fittings and improvements which form part of the building e.g. balconies, shared water pipes, sewage pipes and electrical conduits.

If in doubt, your clients’ original strata management plan and any subsequent by-law or rule amendments will define what is and isn’t common property.

Common Contents includes any appliances, equipment, furniture, fittings and works of art in common areas for which the OC is responsible.

Public Liability is also covered under Strata Insurance, protecting the OC against third party claims for property damage and personal injury in common areas.

2. Contents Insurance

As far as the personal assets belonging to your clients or their tenants are concerned, the cover afforded by a Strata Insurance policy ends as soon as they cross the threshold of their front door and step into their individual lot.

If your clients are Owner-Occupiers or tenants in a strata title, they will need to take out a Contents Insurance policy. This policy is designed to protect their personal assets, as well as any associated public liability risks within their home.

Tip: An easy way to visualise the tangible assets your clients need to personally insure, is to imagine the building being turned upside down and shaken vigorously. Anything that falls out of their lot is their responsibility to insure e.g. clothing, jewellery, furniture and electrical appliances not fixed into the premises.

Internal carpets, light fittings and blinds might not be so easily shaken out, but these items are still included under a Contents Insurance policy, as they do not form part of the building structure.

3. Landlord Insurance

If your clients’ strata property is an investment which they lease, then they’ll need a Landlord Insurance policy.

Landlord Insurance provides cover for the landlord’s fixtures and fittings, including blinds, carpets and light fittings inside the lot. It can also cover rent default and public liability exposures for your clients’ capacity as a landlord.

Should the premises become uninhabitable due to contents damage, the Landlord Insurance policy can also extend to cover Loss of Rent.

To put this insurance jargon into context, let’s look at a claims scenario, explaining how each of these policies responds.

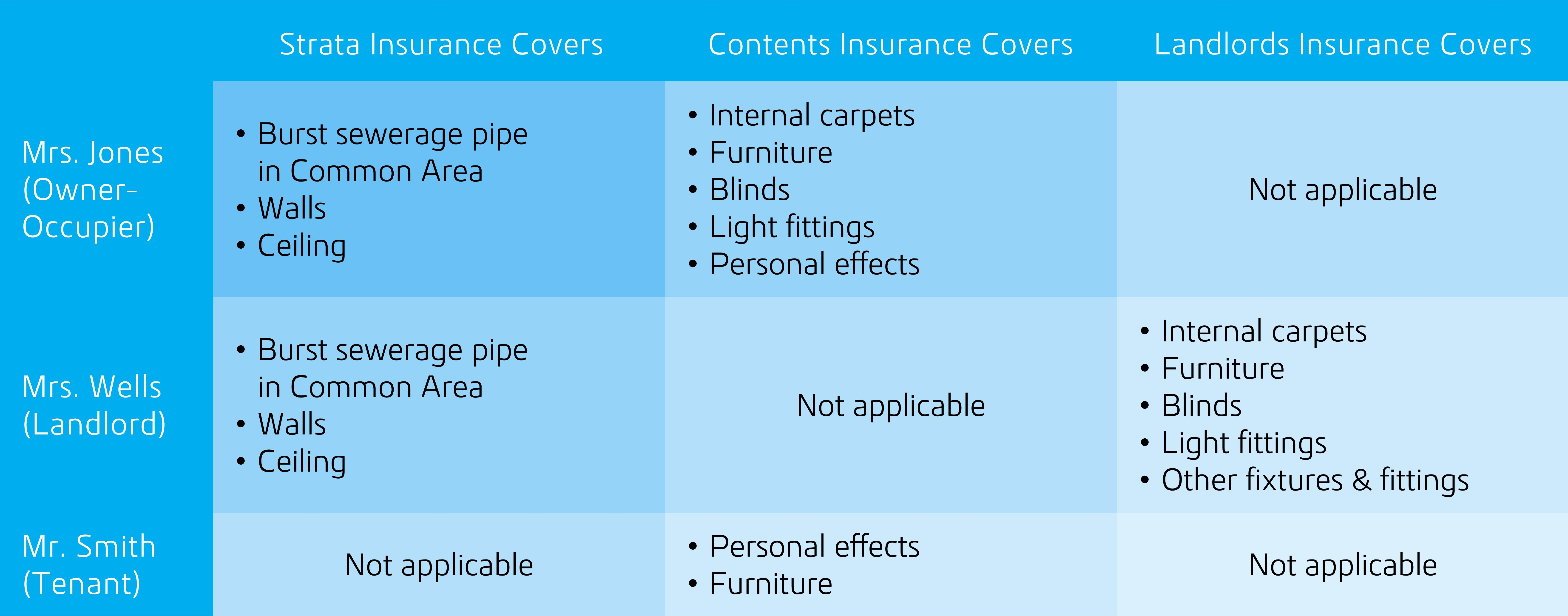

Kings Landing is a residential apartment block comprising 30 separate lots. Mrs. Jones, who lives on Level 5, is an Owner-Occupier. She lives directly above Mr. Smith on Level 4, who is renting the apartment from a private landlord, Mrs. Wells.

One day, Mr. Smith returns from work to discover sewage leaking from his ceiling and his lounge room flooded. It turns out a pipe burst in Mrs. Jones’ apartment, which is causing sewage to seep through the floor and into Mr. Smith’s apartment. Mrs. Jones has extensive damage to her walls, carpets and personal belongings as a result of the burst pipe, as does Mr. Smith.

Mr. Smith, being a tenant, refers the matter immediately to his landlord, Mrs. Wells, informing her that the apartment is uninhabitable until repairs are carried out. Mrs. Wells is concerned that she will be out of pocket for the rent she would have received during the period the repairs are being carried out.

Question:

Who is responsible here? Is it Mrs. Jones’ fault because the problem began in her apartment? Is it the OCs’ responsibility as the sewerage pipe formed part of the building structure? Or, does the answer (as it usually does) lie somewhere in the middle?

Answer:

As the problem occurred in Mrs. Jones’ apartment, Mrs. Jones as an Owner-Occupier would first make a claim under the Strata Insurance policy for the burst sewerage pipe, which is considered Common Property.

The Strata Insurance policy in place for Kings Landing would then respond to cover the repair of the burst sewerage pipe in the Common Area and the repairs of ceilings, walls, etc. for both Mrs. Jones and Mrs. Wells. Mrs. Jones would also make a claim under her Contents policy for the repair and replacement of any contents damaged; this would include damage to carpets.

Mrs. Wells’ structural repairs would be covered under the Strata Insurance policy but she would also need to make a claim under her Landlord policy to repair and replace any carpets, blinds or light fittings damaged.

As the premises has become uninhabitable due to damaged contents, Mrs. Wells’ Landlord policy should respond to cover the rent she will be out of pocket for during the period the premises is uninhabitable.

Mr. Smith would make a claim on his Contents policy to replace and / or repair any of his personal belongings that were damaged.

Strata Insurance isn’t enough on its own.

In summary, Strata Insurance provides critical protection for your clients’ home and / or investment property, but is not sufficient by itself.

Had Mrs. Jones and Mrs. Wells wrongly assumed their contents and / or fixtures and fittings were covered under the Strata Insurance policy, they would have suffered a significant uninsured loss, incurring costs to replace damaged items.

Insurance is complex, and it is rare that one solution fits all situations. The advice above is general in nature and we strongly recommend consulting a professional insurance broker to ensure your clients’ assets are sufficiently protected.

Summary of how each policy responds in the Strata claim example:

Note: The above table applies specifically to the hypothetical situation described in the body of this article. Different policies and circumstances may result in different coverage.

Click here to download a copy for your clients.

For more information on the policies which can best protect your clients’ assets, please contact your Resolute Property Protect Account Manager on 1300 668 033.

This insight article is not intended to be personal advice and you should not rely on it as a substitute for any form of personal advice. Please contact Resolute Property Protect ABN 53 157 850 827 Licence Number: 425966 for further information or refer to our website.